#Associations

Results of the 18th ITMF Global Textile Industry Survey

Consequently, demand soared, and brands and retailers increased orders to meet this pent-up demand. With inflation rising, especially after the Russian invasion of Ukraine in February 2022, demand for consumer goods slowed while inventories remained very high.

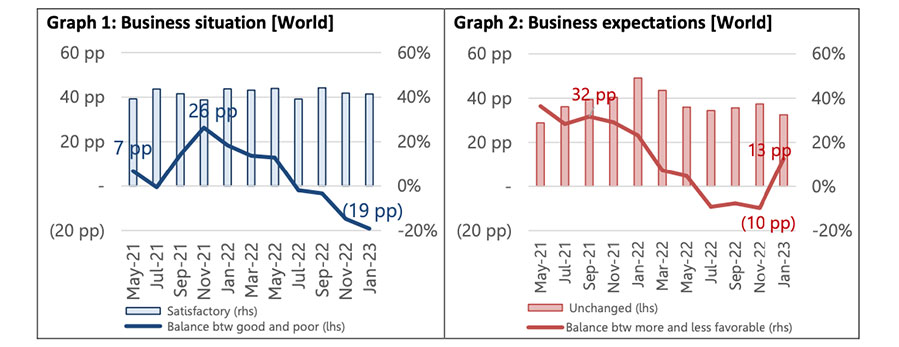

Business situation: gloom – Expectations: boom

Respondents to ITMF’s 18th GTIS survey confirm that order intake has continuously decreased since November 2021. In January 2023, the indicator was negative in all regions and segments except for North & Central America and fibre producers. The latter saw orders rise for the first time since last summer. The previously high global order backlogs also steadily decreased from 3.1 months in March 2022 to 2.4 months in January 2023, mainly due to brand and retailers’ restraint to place orders. The dampening effects of the earlier supply chain disruption further helped reducing order backlogs by improving global trade flows which led to slight rise of the capacity utilisation rate worldwide (mostly driven by fibre producers and spinners).

Expectations in 6 months-time have soared and respondents are globally positive about business in June 2023. Textile manufacturers expect a better situation due to two important factors. First, the world is now in a much better energy situation with a relative mild winter in Europe and energy prices in Europe and Asia (especially for gas) dropping back to levels seen before Russia’s invasion of Ukraine.

Second, the sudden end of the Zero-Covid-policy in China with a swift opening of the borders is promising to strengthen demand in China as well as abroad (more tourists and imports of goods). Everything else being equal, the global economy will see a higher growth level than expected and this will benefit the global textile industry.

For more information, please see www.itmf.org or contact secretariat@itmf.org.