#Raw Materials

High prices persist despite rising stocks outside of China

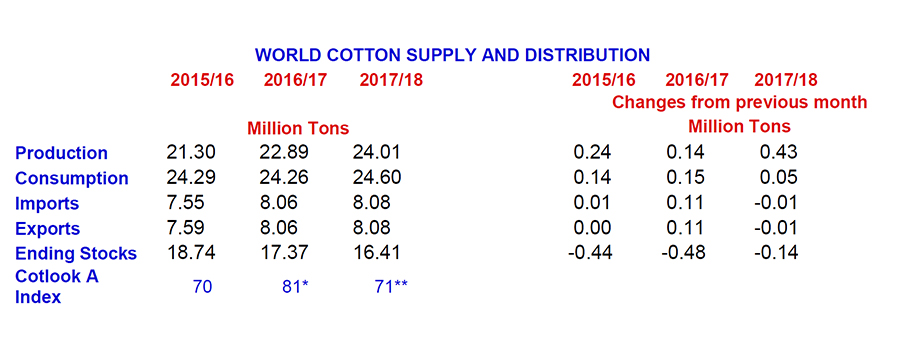

** The price projection for 2016/17 is based on the ending stocks to mill use ratio in the world-less-China in 2015/16 (estimate), 2016/17

In 2016/17, world cotton production is estimated at 22.9 million tons while world mill use is projected at 24.3 million tons, which represents the second consecutive season where mill use has exceeded production. As a result, world ending stocks are forecast to decrease by 7% to 17.3 million tons.