#Digital Printing

Industrial printer shipments show modest decrease in Q1 2022, according to IDC

"Shipments at the beginning of the year started off relatively soft," said Tim Greene, research director, Hardcopy Solutions at IDC. "The market is wrestling with supply chain challenges, war, and pandemic that all contribute to inconsistencies in efficient supply and demand cycles."

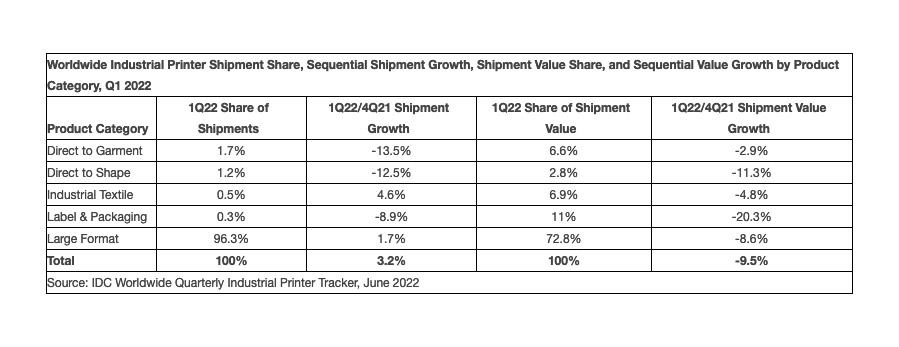

Worldwide Industrial Segment Highlights for Q1 2022

- Large format digital printer shipments make up the bulk of industrial printers and declined by less than 2% in 1Q22 compared to Q4 2021.

- Dedicated direct-to-garment (DTG) printer shipments declined again in 1Q22 despite some strong numbers at the high end of the market. The replacement of dedicated DTG printers with aqueous direct-to-film printers continues.

- Direct-to-shape printer shipments declined 12.5% quarter over quarter in 1Q22.

- Digital label & packaging printer shipments declined 8.9% sequentially in 1Q22.

- Industrial textile printer shipments were a bright spot, growing 4.6% worldwide compared to Q4 2021.

Regional Analysis

- Shipments were down by almost 25% in the Central European market as a result of the war in Ukraine. Many industrial printer manufacturers have suspended activities in the region.

- The strongest growth was in the Japanese market, where shipments grew more than 20% year over year.

- Shipments in North America grew 4.5% for the quarter while shipments in Western Europe grew 3.5%.

- The Asia/Pacific region declined by more than 5% as the region continues to deal with high levels of the pandemic.

Outlook for 2022

Supply chain challenges, the ongoing pandemic, and the Russia-Ukraine war combined to drive industrial printer activities lower in key areas. The resumption of trade shows, the drive for sustainable textile printing, and the reopening of retail are still driving demand.

IDC's Worldwide Quarterly Industrial Printer Tracker provides total market size and vendor share for five major market categories: large format, label and packaging, direct to garment, industrial textile, and direct to shape. In addition to units, shipment value, and average selling price (ASP), the Tracker also provides market results for each product category by ink type, media size, hardware class, or primary application across nine geographic regions and 90 countries.