#Digital Printing

IDC Industrial Printer Tracker finds mixed results in the second quarter of 2021

"Overall large format and industrial printer shipments declined slightly – less than 3% – in the second quarter, largely due to the presence of the COVID-19 delta variant and ongoing supply chain issues," said Tim Greene, research director, Hardcopy Solutions at IDC. "While these factors slowed the recovery that we had seen for three consecutive quarters, some segments still showed excellent growth in Q2 2021."

Worldwide Industrial Segment Highlights for Q2 2021

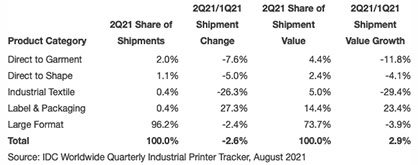

• Large format printer shipments were down 2.4% in 2Q21 compared to the first quarter but were still well above 90,000 units for the quarter on a worldwide basis.

• Direct-to-garment and direct-to-shape printer shipments declined by 7.6% and 5.0% respectively after a very strong first quarter.

• Label & Packaging printer shipments grew by more than 27% in the quarter.

• Industrial Textile printer shipments declined 26.3% in 2Q21 compared to 1Q21.

Regional Analysis

• Total shipments in North America grew 11.6% in 2Q21 compared to the previous quarter.

• Printer shipments in Europe, the Middle East, and Africa (EMEA) declined 8.5% compared to the first quarter. Within the region, slower shipments in Western Europe offset gains in the Central & Eastern European regions.

• Total shipments in Japan were down nearly 25% compared to 1Q21 as the country continues to deal with the coronavirus.

• Shipments in China showed modest sequential growth of 3% in 2Q21.

Worldwide Industrial Printer Shipments and Shipment Value Share and Sequential Growth, Q2 2021

Outlook for 2021

• Investments in new technology that can replace the production capacity of several older devices with greater levels of automation is one of the trends IDC is watching for the second half of 2021 and beyond.

• Despite clear indicators of demand for more digital print solutions, the lingering impact of the pandemic creates a lack of real visibility at either the regional or segment level. Nevertheless, IDC continues to expect the combination of greater demand for new technology, more automated solutions, and more sustainable operations to fuel investments through the end of 2021.